VA Home Loans: Simplifying the Home Buying Process for Military Personnel

VA Home Loans: Simplifying the Home Buying Process for Military Personnel

Blog Article

Taking Full Advantage Of the Perks of Home Loans: A Detailed Technique to Securing Your Perfect Residential Property

Navigating the facility landscape of home fundings calls for a methodical approach to ensure that you protect the home that lines up with your financial objectives. To absolutely make the most of the benefits of home finances, one must consider what steps follow this fundamental job.

Comprehending Home Mortgage Basics

Comprehending the fundamentals of mortgage is important for any individual taking into consideration buying a building. A home loan, usually referred to as a mortgage, is a monetary item that enables individuals to borrow money to acquire realty. The consumer consents to pay back the finance over a defined term, usually ranging from 15 to thirty years, with passion.

Trick elements of home finances include the primary quantity, rate of interest, and payment routines. The principal is the quantity obtained, while the rate of interest is the price of loaning that quantity, revealed as a percent. Rate of interest prices can be dealt with, remaining consistent throughout the car loan term, or variable, rising and fall based on market conditions.

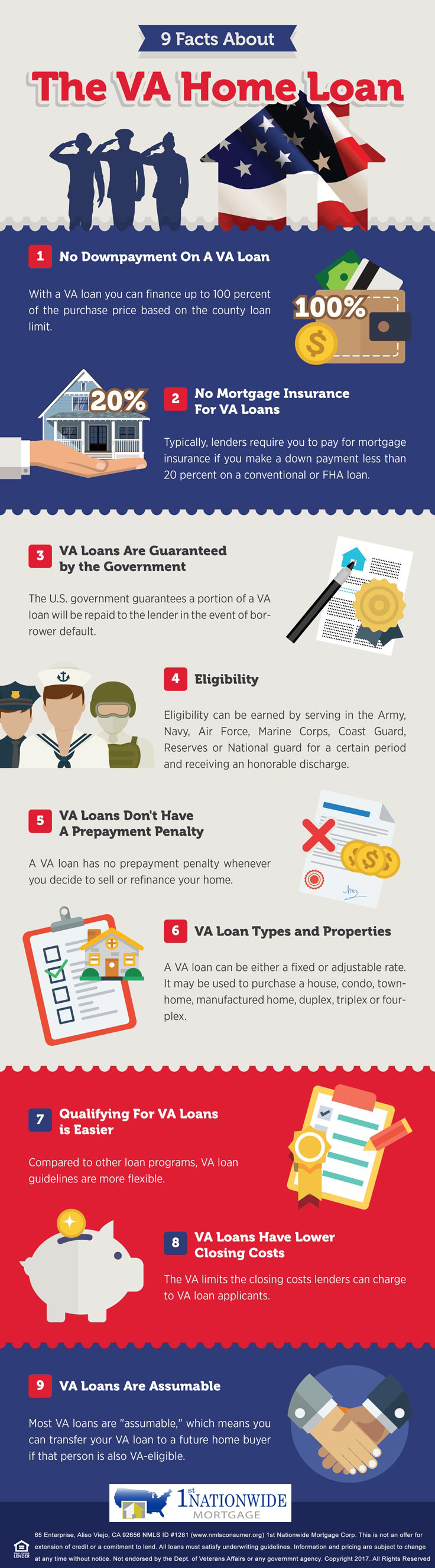

Additionally, consumers should be mindful of different kinds of home lendings, such as standard loans, FHA loans, and VA lendings, each with distinct qualification criteria and benefits. Understanding terms such as deposit, loan-to-value proportion, and exclusive home mortgage insurance (PMI) is also critical for making educated decisions. By understanding these essentials, prospective homeowners can navigate the intricacies of the home loan market and identify alternatives that straighten with their monetary objectives and residential or commercial property ambitions.

Evaluating Your Financial Situation

Assessing your monetary scenario is an essential action prior to starting the home-buying journey. This analysis includes a thorough examination of your income, costs, cost savings, and existing financial debts. Begin by computing your complete regular monthly earnings, consisting of incomes, incentives, and any type of added sources of profits. Next, checklist all monthly expenditures, guaranteeing to represent fixed prices like rent, energies, and variable costs such as grocery stores and entertainment.

After establishing your revenue and expenses, determine your debt-to-income (DTI) proportion, which is essential for loan providers. This proportion is calculated by dividing your complete monthly financial obligation payments by your gross regular monthly earnings. A DTI ratio below 36% is normally considered desirable, indicating that you are not over-leveraged.

In addition, evaluate your credit rating, as it plays a pivotal role in securing beneficial lending terms. A higher credit history can lead to lower rates of interest, ultimately conserving you money over the life of the funding.

Discovering Finance Alternatives

With a clear image of your economic situation developed, the following action involves exploring the various financing options offered to prospective homeowners. Recognizing the different kinds of mortgage is important in picking the appropriate one for your requirements.

Traditional loans are typical financing methods that usually call for a greater credit history and down settlement but deal competitive you could try these out rates of interest. Conversely, government-backed finances, such as FHA, VA, and USDA car loans, deal with certain teams and usually require reduced down settlements and credit report, making them available for first-time customers or those with limited funds.

One more alternative is adjustable-rate home mortgages (ARMs), which include lower preliminary rates that adjust after a specified duration, potentially bring about significant financial savings. Fixed-rate home mortgages, on the various other hand, give security with a regular rate of interest throughout the financing term, protecting you against market changes.

In addition, consider the funding term, which commonly ranges from 15 to three decades. Much shorter terms might have greater regular monthly settlements however can save you passion with time. By carefully evaluating these alternatives, you can make an enlightened decision that aligns with your economic goals and homeownership goals.

Preparing for the Application

Successfully preparing for the application process is crucial for protecting a home finance. A strong credit score is crucial, as it affects the lending click here for more info amount and rate of interest prices offered to you.

Following, gather essential documentation. Common demands consist of current pay stubs, income tax return, bank declarations, and proof of properties. Organizing these files ahead of time can substantially expedite the application procedure. Furthermore, consider getting a pre-approval from loan providers. This not just gives a clear understanding of your loaning capacity but additionally reinforces your placement when making an offer on a residential or commercial property.

Furthermore, establish your spending plan by considering not simply the lending amount but additionally real estate tax, insurance, and maintenance costs. Familiarize yourself with different finance types and their particular terms, as this knowledge will certainly equip you to make enlightened choices during the application process. By taking these positive actions, you will certainly enhance your readiness and increase your opportunities of safeguarding the mortgage that finest fits your requirements.

Closing the Offer

Throughout the closing conference, you will certainly examine and sign numerous records, such as the finance estimate, closing disclosure, and mortgage agreement. It is important to extensively recognize these papers, as they detail the financing terms, repayment schedule, and closing expenses. Make the effort to ask your lender or property representative any inquiries you might need to prevent misunderstandings.

When all files are signed and funds are transferred, you will certainly receive the secrets to your new home. Remember, shutting expenses can differ, so be prepared for costs that might include evaluation costs, title insurance policy, and attorney fees - VA Home Loans. By remaining arranged and informed throughout this procedure, you can make sure a smooth change into homeownership, maximizing the benefits of your home mortgage

Final Thought

Finally, taking full advantage why not check here of the advantages of home mortgage demands an organized method, including a thorough analysis of economic conditions, exploration of varied loan options, and precise prep work for the application process. By sticking to these actions, prospective house owners can boost their opportunities of protecting beneficial financing and achieving their residential property possession objectives. Eventually, cautious navigation of the closing procedure additionally solidifies an effective transition right into homeownership, guaranteeing long-lasting financial security and contentment.

Navigating the facility landscape of home finances requires a methodical strategy to guarantee that you secure the residential or commercial property that aligns with your financial objectives.Recognizing the basics of home financings is important for anyone considering buying a residential property - VA Home Loans. A home funding, typically referred to as a home mortgage, is a financial item that enables individuals to obtain cash to get real estate.Furthermore, debtors must be conscious of different types of home fundings, such as traditional car loans, FHA financings, and VA fundings, each with distinctive eligibility standards and advantages.In verdict, maximizing the advantages of home finances requires a systematic method, incorporating a comprehensive assessment of monetary circumstances, expedition of diverse financing options, and thorough preparation for the application process

Report this page